Actively Managed Funds, Hedge Funds, AI, ML, and now... Robo-Advisors!

Robo-Advisors: Fancy Term to describe something eating up your nest egg without you even noticing it! Another way of thinking of it is that, the more you invest with Robo, the less there's for You

What is a Robo-Advisor?

Robo-Advisors automate investment management by using computer algorithms to build you a portfolio and manage your assets based on your goals and your tolerance for risk.

Robo-Advisors available in Singapore

There are a number of robo-advisors that have come up in Singapore since 2016-17 built on the model of Betterment and Wealthfront in the US promising low cost diversification to investors by investing in overseas (typically the US market) for fees supposedly ranging from 0.5% - 1%. We will see later that it is not true.

Some of the robo-advisors currently active as of 2019 include:

Stashaway

Autowealth

FSM MAPS

Smartly

Philip Smart Portfolio

Kristal.AI

Syfe

Squirrel Save

Some banks have also launched robo-advisor services to various consumers although the fees tend to be a little higher. Some examples include:

OCBC Roboinvest

UTrade Robo

DBS digiportfolio (limited to high net worth investors for now)

Connect by Crossbridge (also limited to HNIs only)

Investors also have access to Dimensional Fund Advisors as of 2019 through various full service, financial advice platforms such as:

Endowus

MoneyOwl

Providend

Breakdown of Fees with StashAway

Quick example with Stashaway

Their yearly fees start at 0.80%

On top of the above, their charges are 0.10% commission fees

All that excludes fees to the ETF manager (~0.30%, i.e. 0.20% - 0.40%) and forex transaction fees if any.

So in conclusion, the yearly fees (i.e. money that you let go) start around 1.20%.

This is insane!!

For $25K invested, you let go 1.2% every year, i.e. $300.

For $50K invested, you let go 1.1% every year, i.e. $550.

For $100K invested, you let go 1.0% every year, i.e. $1000.

For $250K invested, you let go 0.9% every year, i.e. $2,250.

For $500K invested, you let go 0.8% every year, i.e. $4,000.

And obviously, the more you invest in such platform, the more you lose, and the less you earn! (Even though the annual fees are decreasing)

“I know I’m loosing a lot, but I like the simplicity. They invest for me. I don’t need to get worried about anything.”

The simplicity of being stolen money you mean? Who would want to give away so much money for no reason?

The answer: Investors who wish to not do DIY. And this can be understood when you do not have the knowledge, nor the confidence to DIY. No offence here, we all start somewhere! But you must learn how to DIY. That’s the only way.

I’m being a little bit harsh on purpose here, because using Robo-advisor is actually better than doing nothing. It is usually even better than investing in an endowment plan, remember my previous newsletter “Why You Should Never Ever Invest in an Endowment Plan” ?

But, there is muuuuch better to do, because when we analyze the impact of fees over 10, 20, or 30 years, you will never believe it and will probably faint.

There is an inherent conflict in the system

The largest financial institutions are set up to make a profit for themselves.

Not their clients. And guess who is their clients? You!

You may think you are paying fees for high-quality, unbiased advice. This is wrong!

Myth: “Our Fees? They’re a small price to pay!”

Let me start with an example which I believe is pretty close from the real life:

Three friends: Jason, Matt, Taylor

Age: 35 years old

They all have $100,000 to invest

They select 3 different mutual funds with equal performances of 7% p.a.

At age 65 (i.e. 30 years later), how much do they have?

Same investment amount, but Taylor has almost twice as much as Jayson!

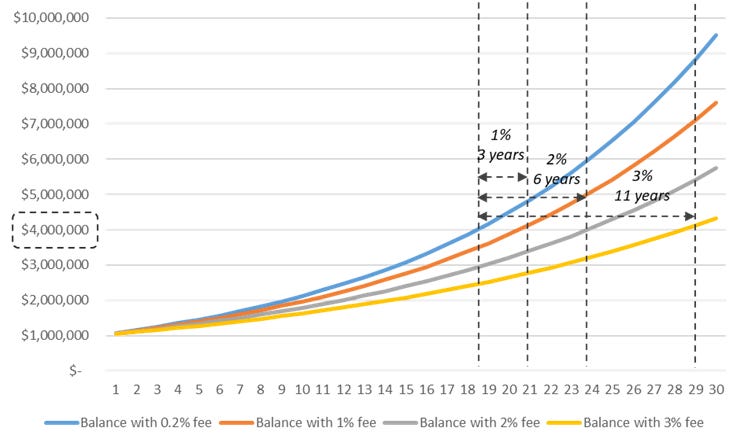

Now, let me show you some examples with the impact of fees on your nest egg, with 0.20%, 1%, 2% and 3% annual fees.

Hypothetical example with $1M invested over 30 years:

What is the outcome?

Overpaying 1% will cost you 3 years’ worth of retirement income

Overpaying 2% will cost you 6 years’ worth of retirement income

Overpaying 3% will cost you 11 years’ worth of retirement income

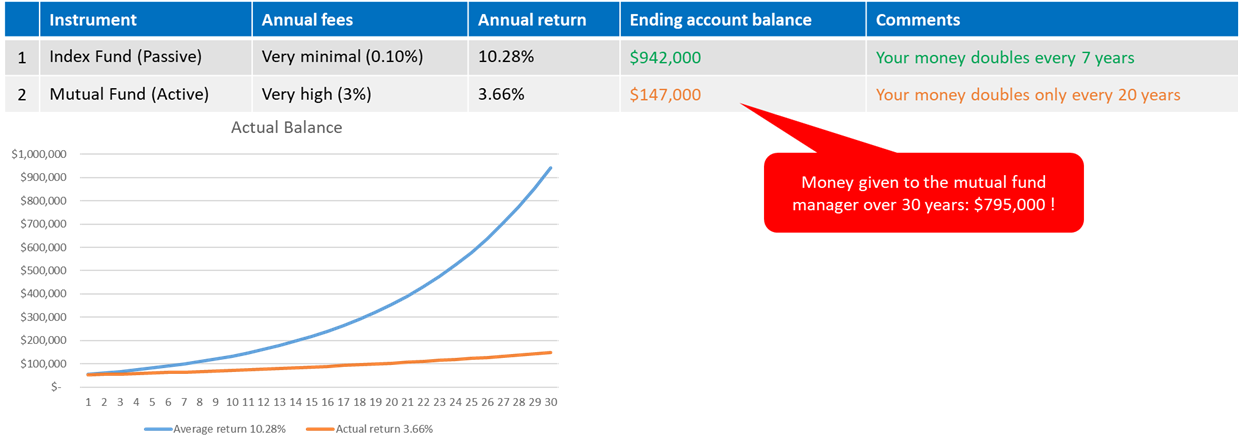

Another example with an average annual return of 10% from 1985 to 2015

Let’s say you’d invested $50,000 in 1985.

After those 30 years, you would end up with:

So instead of ending with $942K, you would only end up with $147K if you fees were 3% p.a., vs 0.10% when DIY.

Know the rules before you get in the game

Most people don’t do the math, and the fees are hidden.

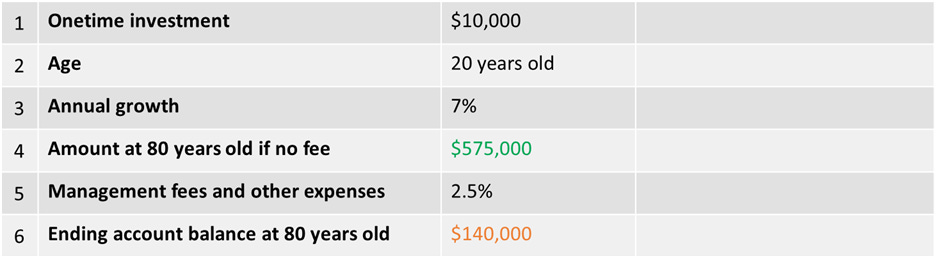

Let me take another example with 2.5% of management fees and other expenses.

You provided all the capital and took all the risk, but you gave exactly 77% of your money to the manager, leaving you with 23% only!!

You put up the capital, you took all the risk

And they made money no matter what happened!

Giving up a disproportionate amount of your potential return to fees is just one of the pitfalls you must avoid if you plan on winning the game.

Today, the only way to become rich, is to DIY

You will only become wealthy if you DIY. This will allow you to pay not even 0.20% of fees p.a. Remember, in Investing, You Get What You Don’t Pay For!

You cannot trust any actively managed funds, nor robo-advisors.

They are just here for your money. You are the product.

Your fund manager, your financial “advisor” will end up with a yacht, not you.

If you want to change that, if you want to change the paradigm, just DIY.

Don’t hesitate to contact me at thibault.morisse@gmail.com if this newsletter caught your interest :-)

You liked this post? Share it!

You didn’t subscribe to “Investing Mad(e) Easy” Newsletter yet? Click here!

You like “Investing Mad(e) Easy”? Share it too!

*Disclaimer: “Investing Mad(e) Easy” newsletter is not intended to be and does not constitute financial advice, investment advice, trading advice or any other advice or recommendation of any sort. More info here*