[Investing Made Easy] Why You Should Never Ever Invest in an Endowment Plan

[Investing Made Easy] Why You Should Never Ever Invest in an Endowment Plan

You recently opened an Endowment Plan? Run away from it! Or you may be thinking opening one? Think twice and don't do it! But why? Simple: this product is worse than lousy.

Life Insurance vs. Endowment Insurance

The major difference between life and endowment is that they have two different end goals:

Life insurance covers you mainly for death, terminal illness or disability

Endowment is more of a savings plan with a small life insurance component attached.

All the people that I have been discussing with in Singapore, primarily opened an endowment plan as what they thought would be a great savings plan. Meaning that they never cared about the super tiny life insurance attached to it, since usually, you already have this covered with a dedicated life insurance plan.

Why Endowment plan is crap?

Two main reasons:

The yield is really, really, really low

Between 1.00% (Guaranteed, Short term plan) and 4.75% (Non-guaranteed, Mid-Long term plan)

If you need more info, there are many great websites out there providing an exhaustive list of all the different plans available. For instance, this one.

Your money is blocked for the whole duration of the policy term

What if you urgently need your money at some point in your life, and that you have no EF (Emergency fund) aside?

We will discuss these 2 points below, with actually two different real use-cases from people who got the illusion that Endowment Plan was a great plan.

Both use-cases are - coincidentally - based on Prudential, but with 2 different plans. Let’s analyze them!

Use-Case #1

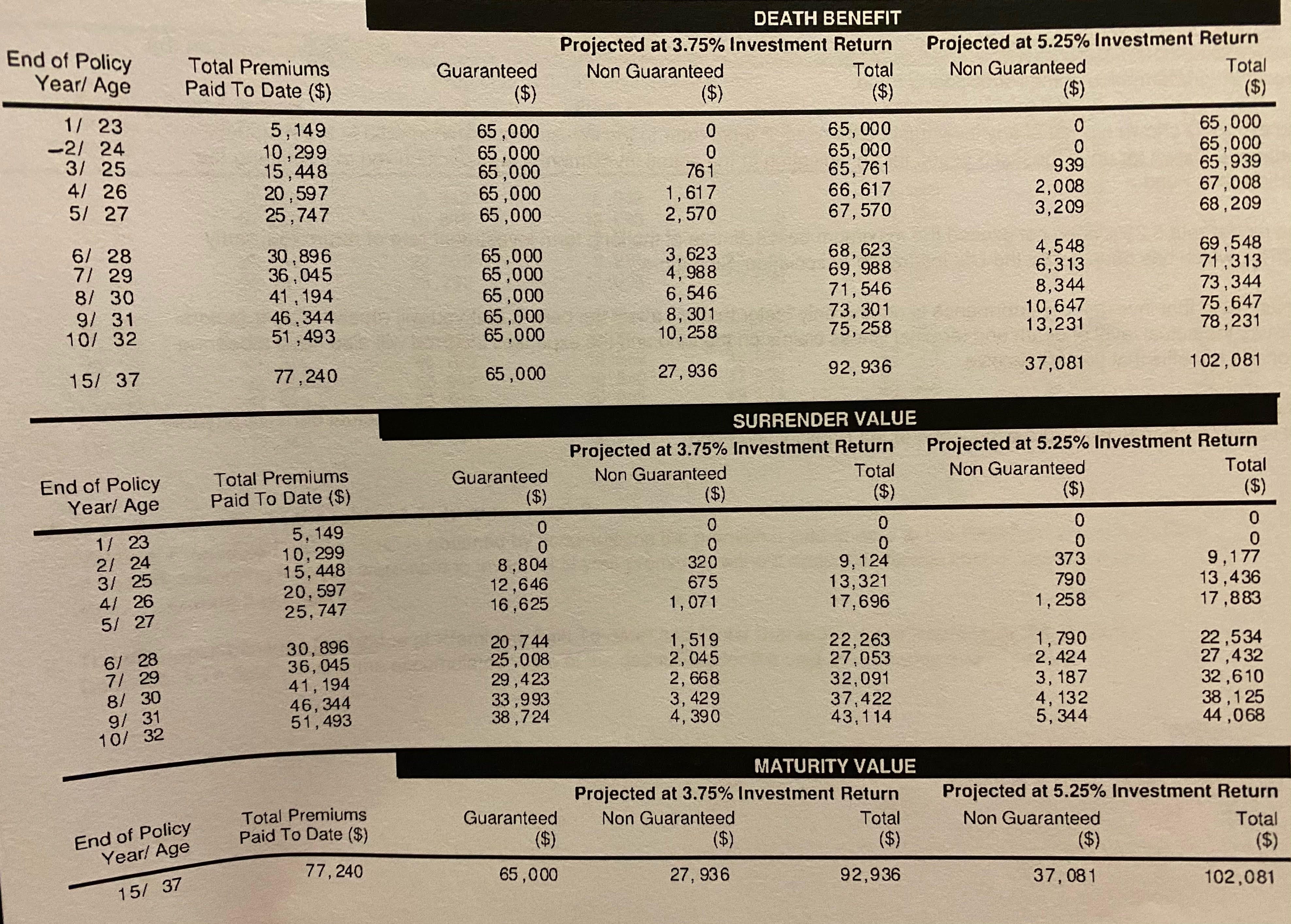

Plan: Prudential PruSave

End of Policy: 15 years

Total Premium Paid: S$ 77,240

Expense Ratio: ~ 0.30% / year

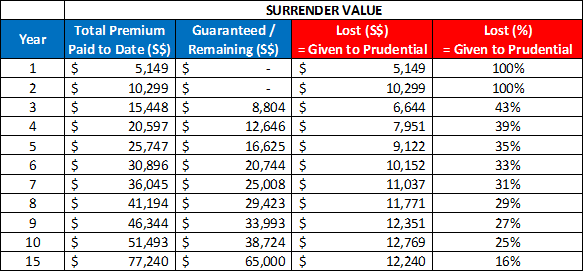

Surrender Value

A quick Excel table clearly shows how you are being ripped off by your insurance company. And don’t worry: they are ALL THE SAME! Don’t think you found a gem, if you have an endowment plan, you’re in this too :-)

The last 2 columns are the most important. It is self explanatory, you don’t need my help here:

Maturity Value

Ahhhh finally the main topic! Remember the 2 projections that Prudential mentioned in their contract, i.e. at 3.75% and 5.25% p.a. ?

But is it really 3.75% and 5.25% p.a.? Or is it much less? Back to Excel!

Projection with 3.75%: Don’t you see an issue here?

How about the projection at 5.25%?

Yes, you’ve - unfortunately - been fooled by your supposedly “advisor”.

Use-Case #2

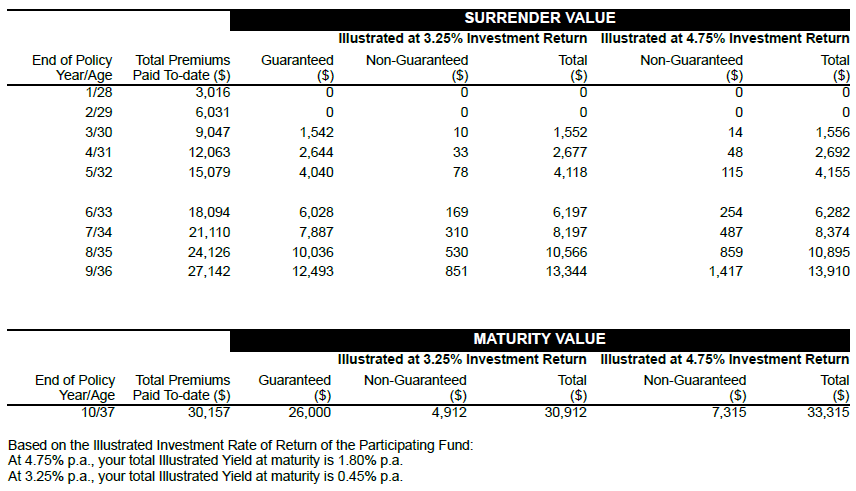

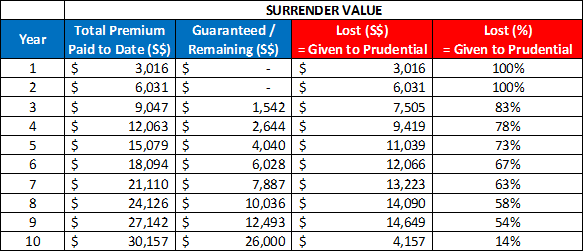

Plan: Prudential PruActive Saver

End of Policy: 10 years

Total Premium Paid: S$ 30,157

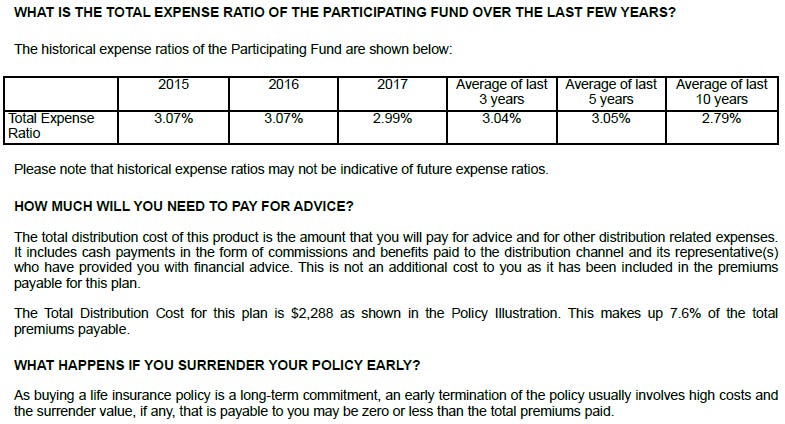

Expense Ratio: ~ 3.00% / year!!

This is just 3,000% (Yes, Three Thousands %) more expensive than the ER of powerful products available out there = 0.10% p.a.

Imagine buying something $3,000 but you can find something much better for $1 only? Which one would you chose?

In finance, you get what you DON’T pay for.

“How much will you need to pay for advice"?”

What? Which advice? And I need to pay S$2,288 to get ripped off! WOW!

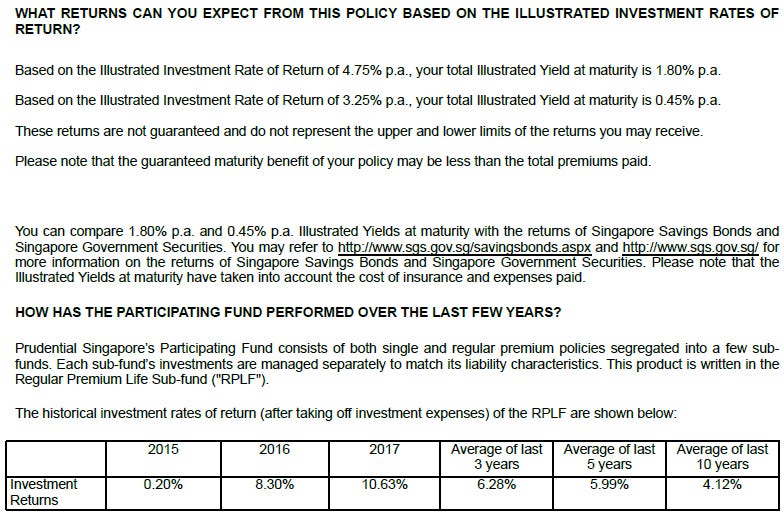

Expected Returns

Surrender Value

Same than for use-case #1, let’s check how it looks like:

Maturity Value

Here again… Is it really 3.25% and 4.75% p.a.? Or is it much less? Let’s work this out again with Excel!

Projection with 3.25%

How about the projection at 4.75%?

“Hold on! First, I’m reading that”

The illustrated rate of return is 3.25%, which leads to a Total Illustrated Yield at Maturity = 0.45%. But actually, the real return NET is only 0.25% ??

The answer is Yes.

The illustrated rate of return is 4.75%, which leads to a Total Illustrated Yield at Maturity = 1.80%. But actually, the real return NET is only 1.00% ??

The answer is - unfortunately here too - Yes.

Conclusion

You’re not dreaming: your endowment plan has a lower yield than a basic DBS Multiplier or UOB One!

On top of this, your money is locked and the surrender clause is just CRAZY.

Why would you want to invest in such a lousy product, especially when you know there are investment products out there that can provide you with an annual average return of 10% in the long run?

Based on the holding year you are in right now, it may be wise to surrender it all and invest in much better product. You are losing your time! Put you pride aside, and if you are still in the very first years on holding, jump out and never ever look back, this will be one of the best decision you will ever make.

The above use-cases are real, and once again, don’t fool yourself: no matter which endowment plan you have, you’re all in the same boat.

If you are looking for great savings plan and amazing - real - returns, stay tuned!

You liked this post? Share it!

You didn’t subscribe to “Investing Mad(e) Easy” Newsletter yet? Click here!

You like “Investing Mad(e) Easy”? Share it too!

*Disclaimer: “Investing Mad(e) Easy” newsletter is not intended to be and does not constitute financial advice, investment advice, trading advice or any other advice or recommendation of any sort. More info here*