The Rule of 72, aka the Power of the Compound Interests, or Snowball Effect

The Rule of 72, aka the Power of the Compound Interests, or Snowball Effect

One day, a genius said: "Compound interest is the eighth wonder of the world. He who understands it, earns it; he who doesn't, pays it."

Disclaimer: Sometimes, Newsletters between Investing Made in France and Investing Made Easy will be extremely similar, not to say identical, for the simple reason that some topics are common, and this cannot be avoided.

This is going to be the case with this current Newsletter, that I have already published last week on Investing Made in France: La règle des 72, ou les intérêts composés

The differences are:

The language used (French vs English)

But also the different kind of investment instruments available (in France vs Singapore)

Let’s get this started

This could also be rephrased this way: small streams become great rivers.

And the yield of this accumulation is way more important than you can ever think of.

Discover the Power of the Compounding Interest with the snowball example.

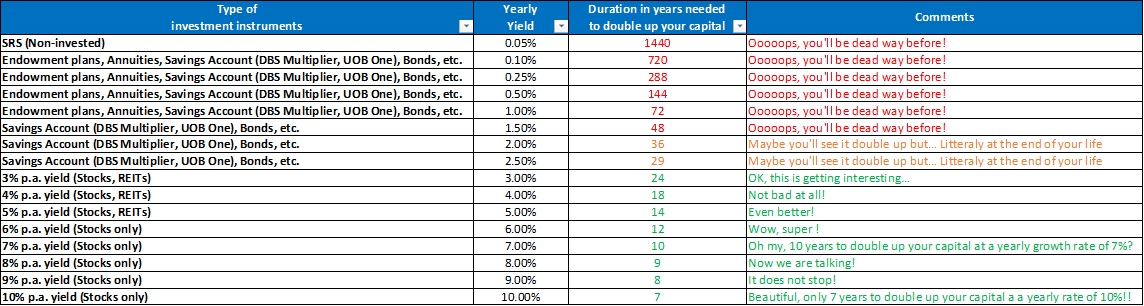

“The Rule of 72. What is it?”

The rule of 72 is a method to estimate the time it takes for a capital to double up.

But how to quickly calculate all of that?

If a capital is invested with an interest rate of t % per period (generally speaking, years), the capital will be doubled up 72/t periods later.

I computed it all for you

You are probably going to be super disappointed and that’s my aim: to give you an electroshock!

Bear in mind that the above tables with regards to “which type of investments = yearly yield” is based on my own expertise and can’t be taken for granted, though I know I am pretty close from the reality for all of them.

Especially for Endowment Plans and Annuities: please refer to my previous newsletter Why You Should Never Ever Invest in an Endowment Plan

You must stop believing the B.S. and the Lies that are sold to you by your supposedly “Financial Advisor”

You will never ever become rich if you only bet on financial products provided by “Agent” or “Financial Advisor”, who are nothing but actually sales people.

So, forget about Endowment Plans, Annuities, Savings Plan (DBS Multiplier, UOB One), Bonds.

However, the paradigm is considerably changing when you start looking at products with a yearly yield that start around 3% p.a. (Pretty safe products), and that go up to 10% p.a. (With a lot more risk however, so this will depend in each and every of your personal situation).

But this is where I wanna catch your attention: It is relatively easy to find products yielding from 3% to 10% p.a., so why not benefit from them?

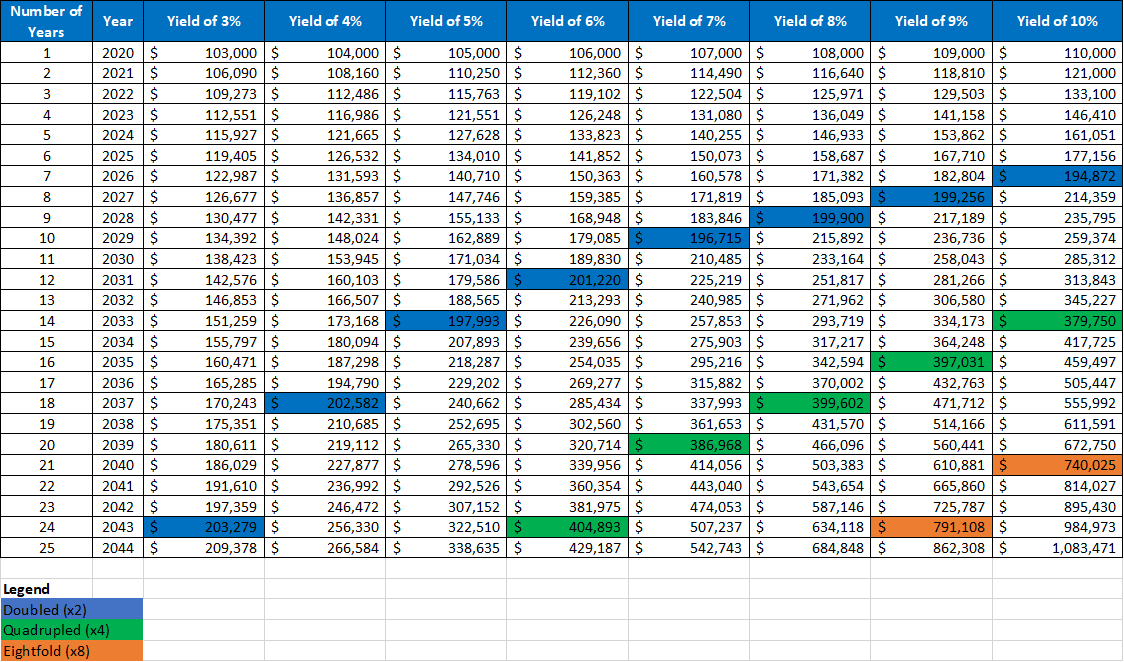

A capital doubled up in X years, is a capital quadrupled (x4) in 2X years, but also increased eightfold (x8), in 3X years.

Concrete example with a starting capital of $100K on 1st January 2020, and without any single top up following up:

Unnecessary to mention products with yearly yield of less than 3% p.a., since you will understand that you won’t even have time to see your capital double up of your living.

So, do you still want to leave all your money rot on:

Non-invested SRS?

Endowment Plan?

Annuity?

Bonds?

Savings Account?

Don’t hesitate to contact me at thibault.morisse@gmail.com if you change your mind. :-)

You liked this post? Share it!

You didn’t subscribe to “Investing Mad(e) Easy” Newsletter yet? Click here!

You like “Investing Mad(e) Easy”? Share it too!

*Disclaimer: “Investing Mad(e) Easy” newsletter is not intended to be and does not constitute financial advice, investment advice, trading advice or any other advice or recommendation of any sort. More info here*