The Truth about the S.R.S aka the Supplementary Retirement Scheme for SP/EP holder (Part 1)

The Truth about the S.R.S aka the Supplementary Retirement Scheme for SP/EP holder (Part 1)

"I discovered something, it is THE BOMB: it is called SRS. It is even available for SP/EP holder! You invest up to S$35K per year, and 10 years later, you only pay income tax on 50%. Amazing!" Or not.

What is SRS?

Unnecessary to introduce the SRS (Supplementary Retirement Scheme) in this newsletter, there are plenty of newsletters, blogs and websites out there talking about that topic.

Is SRS as good as advertised all over Singapore when we are “simple wanderers” (i.e. SP/EP holder) ?

Everyone will sing the praises of this dear SRS, but how many really went to the bottom of it, and were able to tell you:

While SRS is undoubtedly really good for Singapore Citizen or PR holder who will still be PR (or citizen, why not) when the statutory retirement age kicks in (62 years old for now), is it worth investing in the SRS when we are really foreigner, only holding a SP/EP?

While only a SP/EP holder, will you make or lose money if you invest in the SRS?

If you are losing money, after how many years will you break even?

But if you leave Singapore before the 10 years parking period, how will that work out for you?

All these questions are extremely difficult to answer, but not impossible!

It took me days to come out with a fair, complete and precise comparison of ALL the different possible combinations (many many many!), and here we are.

“What if….”

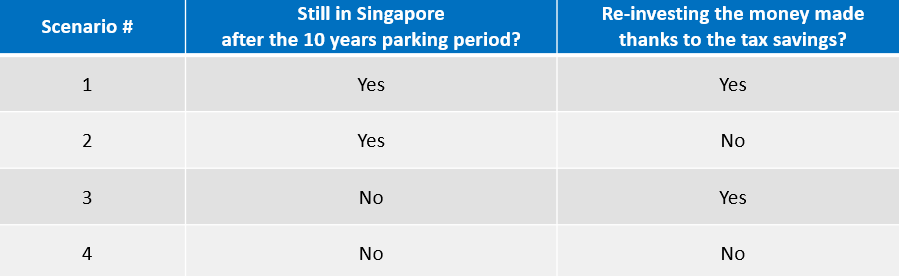

Yes, what if… What if what actually? I am gonna split the outcome based on 4 different scenarios, as follows:

Each scenario will contains sub-scenarios too, but in order to limit the number of possibilities, the only variable will be:

How long are you investing/gonna invest in the SRS for, from 1 to 10 years

Assumptions

Few assumptions had to be made, otherwise, this exercise could be endless:

Each and every year, S$35K are invested in the SRS: not more, not less.

Three different investments rates of return have been used to really assess the situation

Growth of 10% p.a.

Growth of 6% p.a.

Growth of 2% p.a.

If you decide to re-invest the money you are saving thanks to the SRS tax savings, it must be re-invested in the same rate of returns than the money you are investing in your SRS account: 10%, 6% or 2%.

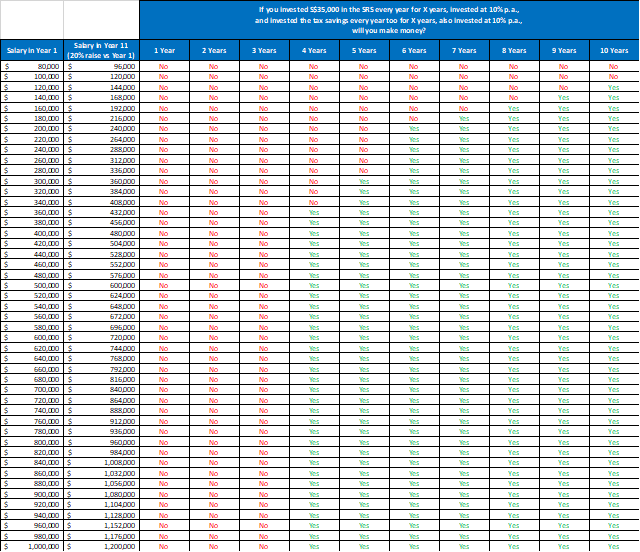

Within the 10 years of SRS holding, your salary will get a 20% raise (i.e. ~ 2% increase p.a. Pretty fair I believe). Meaning in Year 11, once you withdraw all your SRS funds, your income will be 20% higher than in Year 1.

How many different combinations will this lead to?

Let’s recap:

10 years = 10 combinations

3 different rates of return = 3 combinations

4 scenarios = 4 combinations

So I believe, 10 * 3 * 4 = 120 combinations!

This should be enough to assess if SRS is a good deal for you, or not.

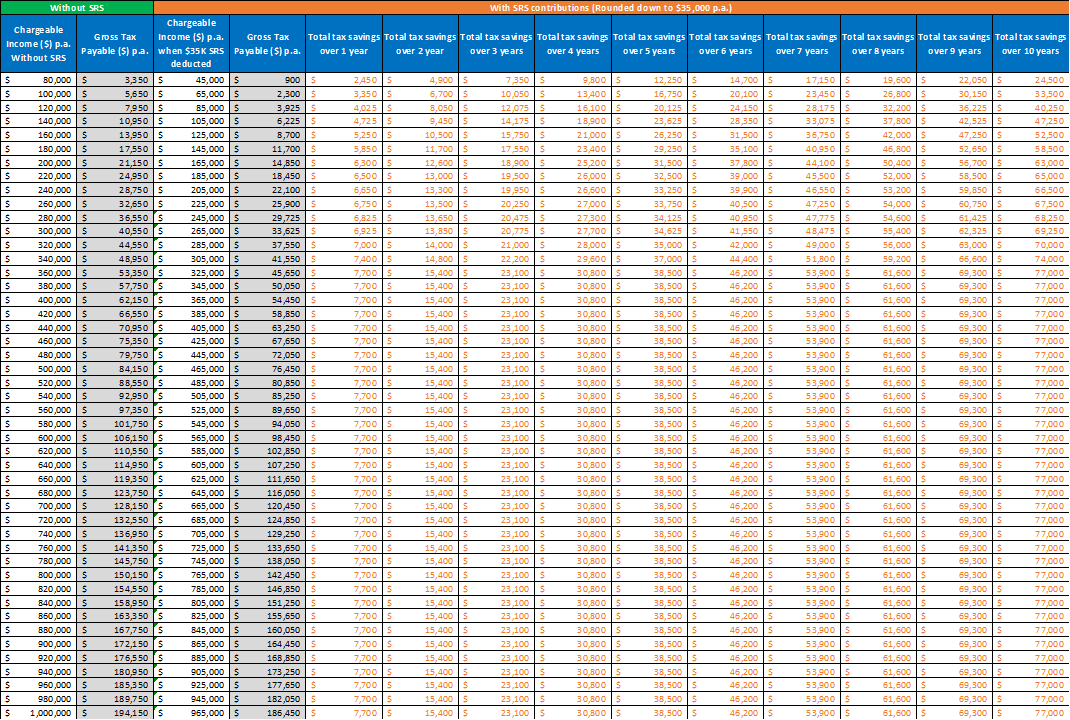

How much tax savings will you benefit from investing in the SRS, based on your salary, from 1 to 10 years?

Minor assumptions for a easier calculation: no income raise for 10 years in this table.

Part #1

We will only cover the first 2 Scenarios, i.e. already 60 combinations.

For both scenarios, you will have to pay your income tax including the entire SRS funds (50% of this money will be taxed) based on the local income tax rate once you are allowed to withdraw the funds from your SRS.

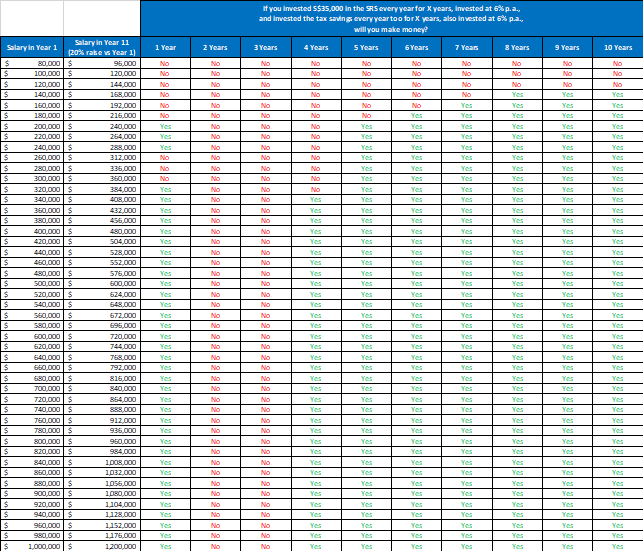

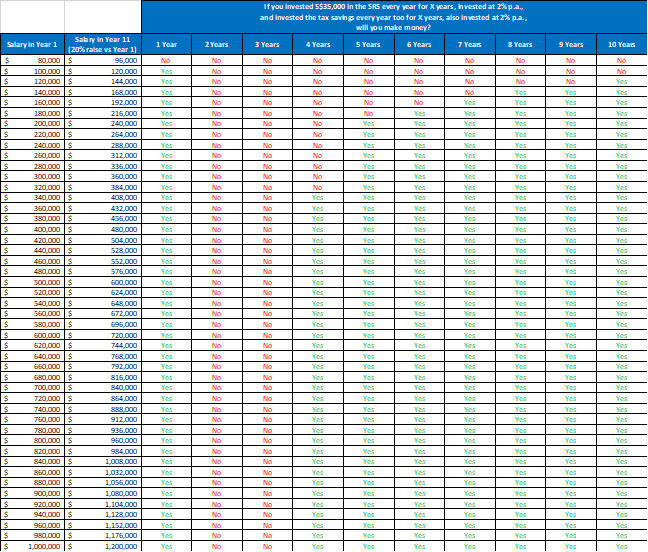

Scenario #1: Still in Singapore after 10 years, and re-investing all the money saved thanks to SRS tax savings

Three sub-scenarios will be presented:

All the money (both $35K SRS + tax savings) invested at 10% return p.a.

All the money (both $35K SRS + tax savings) invested at 6% return p.a.

All the money (both $35K SRS + tax savings) invested at 2% return p.a.

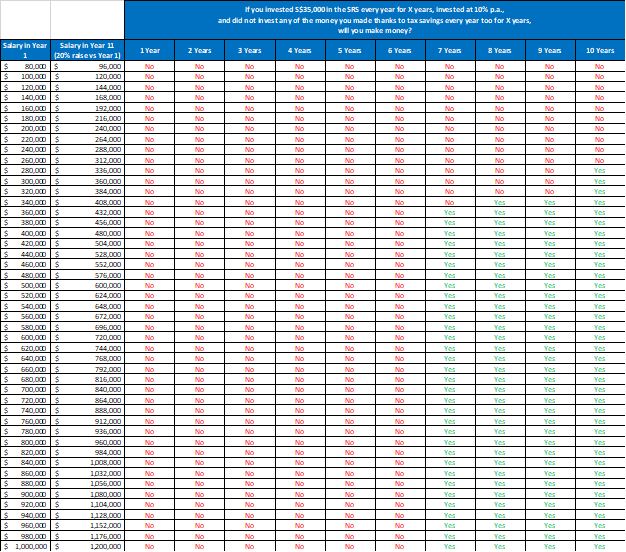

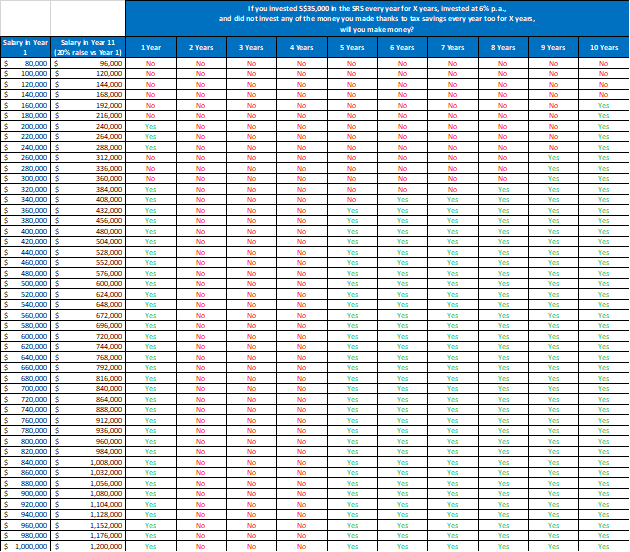

Scenario #2: Still in Singapore after 10 years, but not re-investing any of the money saved thanks to SRS tax savings

Three sub-scenarios will be presented:

The $35K in SRS is invested at 10% return p.a. The tax savings is not invested at all.

The $35K in SRS is invested at 6% return p.a. The tax savings is not invested at all.

The $35K in SRS is invested at 2% return p.a. The tax savings is not invested at all.

Conclusion

It is way too difficult to draw anything!

However, something which is blindingly obvious is that you will always lose money whatever is your salary, if you only invest in your SRS while living, working and paying your tax in Singapore, for less than 4 years.

From the fourth year onwards, SRS becomes interesting, only if you stay in Singapore till the 10 years term, and continue to invest S$35K every year. But you have to have a deep look into the above 6 tables in order to draw your own conclusion.

Conclusion of the Conclusion

If you know that from the moment you WANT to open your SRS, you will not be in Singapore anymore 4 years later, I got only one recommendation for you: do NOT open SRS!

Ask yourself the below questions:

Do you really know where you will end up in 5, or 10 years?

Do you really want to lock your money in for 10 years, with huge penalty if you take out this money before 10 years?

Or do you want to have this money at your disposal anytime, with the freedom to use it whenever you want?

Would you be serious and mentally strong enough to invest the money you saved thanks to the tax savings in order to make your SRS investment become really meaningful, or will you use that money to buy unnecessary things and make your SRS investment becomes weak?

There are so many unknown variables in life, that no one will ever be able to say what the future holds. So, would you really want to get yourself prisoner of your own decision, or do you want to live freely, with all your money available at your fingertips?

What’s in for Part #2?

We will dissect the same than above, the only difference being that we will assume that you are not in Singapore once the 10 years parking period kicks in.

What will be the impact knowing that you will be taxed 15%, which is the non-resident tax rate (Question #19).

Any Questions?

Don’t hesitate to ping me at thibault.morisse@gmail.com if you want to:

Fine-tune the table for you

Know how much money you will win/lose because of your SRS, based on your situation

See the trends/charts based on your salary

You liked this post? Share it!

You didn’t subscribe to “Investing Mad(e) Easy” Newsletter yet? Click here!

You like “Investing Mad(e) Easy”? Share it too!

*Disclaimer: “Investing Mad(e) Easy” newsletter is not intended to be and does not constitute financial advice, investment advice, trading advice or any other advice or recommendation of any sort. More info here*

Full of passion!