Track Record Update: +56%. 3.5 Years.

Track Record Update: +56%. 3.5 Years.

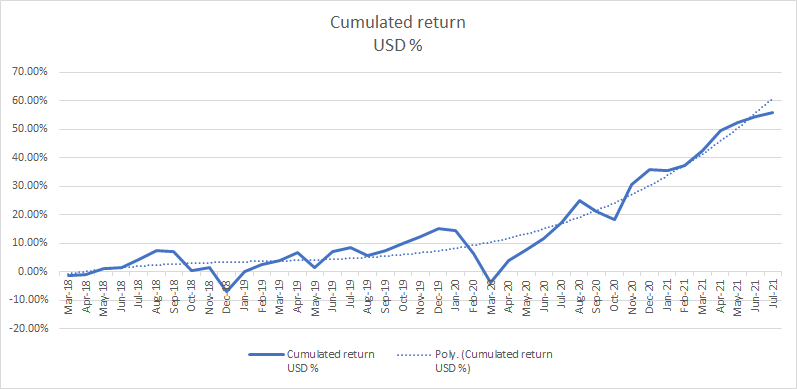

+56% of Cumulated Returns in exactly 41 months. Another way to see it: +14% growth per year.

+56%. 3.5 Years. Let’s decipher the data.

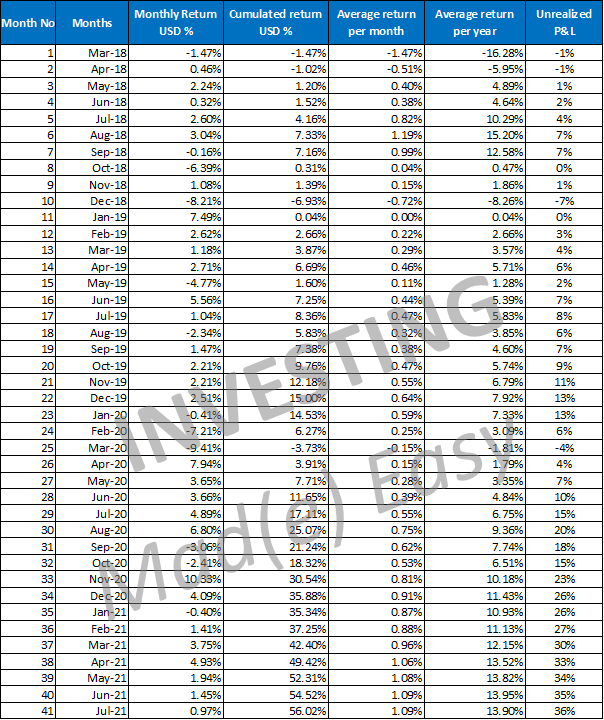

Cumulated Return in % since March 2018: +56%

Average Return per year since March 2018: +14%

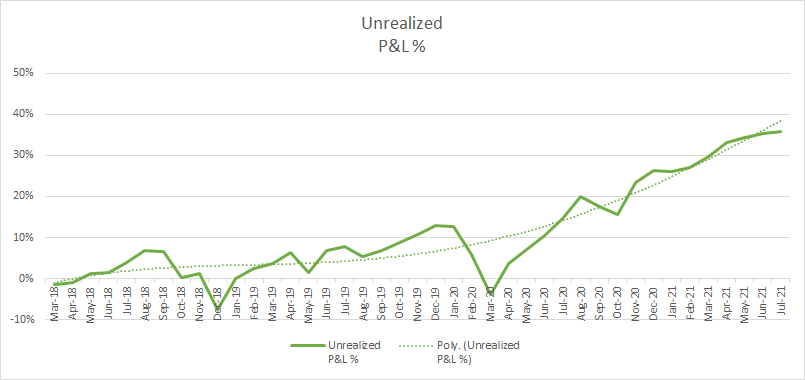

Unrealized P&L % based on the Total Net Liquidity as of 1st August 2021: +36%

It is really important to measure the performances using the "cumulated return" as I am DCA-ing every month. That's the most relevant data you can ever get as the "unrealized P&L %" won’t talk much in that case, since I keep putting every month.

But I will still give you a glimpse at what +36% of P&L based on the Total Nest-Egg Amount looks like ;-)

Below is the table with all the data, throughout all the months since I started one of the most exciting adventure of my life, Investing for my Retirement!

How about the Cumulated Return chart?

And the Unrealized P&L one?

Why using Unrealized P&L not a good idea at all?

Say you have invested $100K in your trading account as of today. Have you really invested this $100K at one go, the very first day you started investing? I doubt so.

All right, that’s it. No simplest explanation than the above can be found.

Joke aside, DCA-ing monthly is like planting seeds throughout months, years, even decades. Early in your career, you may start investing $1K a month. Then slowly, you will increase to $2K. After getting a nice pay rise, you can now invest $5K a month, and so on and so forth.

Because of the above, your unrealized P&L % will keep on evolving and will not be realistic because your investment keeps working, working and working. It’s nothing but a sliding window, an endless Work-In-Progress.

Another way to look at it is, using a very basic example:

Investment Period: 1st January 2020 - 31st December 2020 (1 full year)

Investment return: 10% p.a.

Two investments were made, for a total of $110K

1 January: $10K

31st December: $100K

Then on the 1st January 2021, you decide to check your portfolio performances.

$10K became $11K

$100K is still $100K

Which of the two approaches presented here-above is the most accurate? “Monthly Cumulated Return” or “Unrealized P&L” ?

The compounding effect (Making interests out of interests themselves making interests…. etc.) will never ever stop.

So until and unless you have invested all your money at one go, and stop investing a single penny, you simply can’t use the Unrealized P&L% as an accurate way of calculating the yield/performance of your entire portfolio. In other words, if you use DCA, do not “trust” the “Unrealized P&L” as the Gospel Truth. Simply use it if you want to roughly know where you stand, but without precision.

Using “Unrealized P&L” may motivate you to start investing NOW!

Well, I actually never ever use the Unrealized P&L, but for the sake of today’s newsletter, let me do it with few different use-cases, that I hope will help you understand why you must start to invest NOW.

We will use March 2018 as the time at which one started investing. I will be using 3 simple assumptions, that will allow you to see how much gains we are talking about:

If one has $100K of Net Liquidity today, the total gains are +$36K

If one has $500K of Net Liquidity today, the total gains are +$180K

If one has $1M of Net Liquidity today, the total gains are +$360K

Again, these gains don’t account for all the money you have invested since you’ve started the adventure, as you’ve put some cash 3 years ago, but also last month.

This is the reason why “Time In The Market” is much more important than “Timing The Market”.

In the market to reach +400%

This investment is nothing but my retirement nest-egg. I’m in for the long term: 20, 30 years.

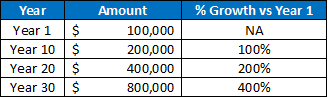

To make it simple, one could see his money doubling (+100%) every 10 years (If 7% p.a. growth). If we are lucky enough, we could see our money grow 100% only after 7 years, if the stock market performance is +10% p.a.

But let’s use the “worst case” scenario with 7%:

Doubling means realizing +100% profits on your investment after a decade.

So after 20 years, your money will grow by 200%

And after 30 years, 100% of 200%, i.e. 400% vs Year 1.

An example with $100K invested at one shot, Year 1, without no other deposits ever for the next 30 years. But we agreed this will not happen, right? You didn’t forget the DCA, did you?

+/- 1% performance tracking accuracy over a year of data is pure noise, regardless the method being used.

Actually, even 10% accuracy error would be ok when your initial investment has grown to +400%. Who would care to get +390%, or +410%?

In The Market I Trust

Being in the market for the long run allows me to be super confident about its outcome. I’ve never been, I’m not, and I will never be shy to invest my hard-earned dollars into the stock market because I have trust in it.

I’m actually fine making “only” +400% gains over 30 years, now that the machine has been fired up. Even if the market drops ~35%, I will still be positive overall.

The future is bright, I am not scared anymore. Whatever amount I now invest in the stock market is pure bonus. And that crazy stuff is good, so why do without it?

The Best Thing to do when investing in the Market?

Invest YESTERDAY!

Not Tomorrow, not Today. YESTERDAY.

KEEP YOUR COSTS LOW. As LOW as possible.

STAY THE COURSE.

Through ups and downs, through thick and thin.

Invest AS MUCH AS YOU CAN, AS EARLY AS YOU CAN

I usually invest ~50% of my pay check.

Thanks to COVID, this is more around 60-65% as we speak.

TIME is your friend.

The Cherry on the Cake: Up to US$1,000 of free IBKR stock when opening an account at Interactive Brokers

If you sign up with my link, you will be offered US$10 of IBKR stock for every $1,000 invested via their platform (Regardless the stocks or ETFs purchased).

The offer is limited to US$1,000 of free IBKR stock if you invest US$100,000.

On top of saving a lot of money, you are also about to make easy money.

Tested working and approved by friends & family.

You liked this post? Share it!

You didn’t subscribe to “Investing Mad(e) Easy” Newsletter yet? Click here!

You like “Investing Mad(e) Easy”? Share it too!

*Disclaimer: “Investing Mad(e) Easy” newsletter is not intended to be and does not constitute financial advice, investment advice, trading advice or any other advice or recommendation of any sort. More info here*